AI Customer Service for Banking and Financial Services: 2026 Guide

AI customer service in banking is no longer a pilot project. Retail banks, credit unions, and wealth management firms are running grounded AI on live tickets, chats, and call transcripts, and the regulators have caught up. The Consumer Financial Protection Bureau (CFPB), Office of the Comptroller of the Currency (OCC), and FFIEC have all issued explicit guidance on how AI can and cannot interact with consumers in regulated financial contexts.

That changes the buying conversation. A banking AI chatbot in 2026 has to do three things at once: resolve a meaningful share of customer questions, refuse to give regulated advice it is not qualified to give, and produce an audit trail that survives a compliance review.

This guide is for VP Customer Experience, Head of Contact Center, and digital banking leaders at institutions large enough to face regulatory scrutiny and small enough that a 9-month vendor cycle is not an option. It covers what AI in banking customer service actually does today, where it breaks, and what to require before you sign a contract.

What Is AI Customer Service for Banking?

AI customer service for banking is the use of large language models, retrieval-augmented generation (RAG), and agentic workflows to answer customer questions, triage tickets, take account actions, and assist human agents inside a regulated financial institution. The category covers chatbots, voice agents, agent assist tools, and back-office automation that touch the customer experience.

The defining constraint is regulation. Generic SaaS AI support has to be accurate and brand-safe. Banking AI customer service has to be accurate, brand-safe, compliant with consumer-finance rules, auditable by examiners, explainable to a regulator, and conservative about anything that resembles financial, tax, or legal advice. That changes how the system has to be built.

Banking AI deployment type | What it does | Regulatory weight |

Customer-facing chatbot | Answers account, product, fee, and self-service questions | High: direct consumer impact |

Voice AI / IVR | Authenticates, routes, and resolves calls | High: recording and consent rules |

Agent assist | Drafts answers, surfaces policy, summarizes calls | Medium: internal but logged |

Ticket triage and routing | Classifies, prioritizes, and assigns | Low to medium |

Back-office automation | Disputes, KYC document checks, fraud notes | High: direct financial impact |

The market is growing fast. Independent forecasts put AI agents in financial services on track to reach roughly $6.54 billion by 2035, and the customer service category is the fastest-moving slice because the use cases are well-defined and the ROI is countable.

Why Banks Need a Different AI Approach Than Generic SaaS

A SaaS company can ship an AI chatbot that occasionally hallucinates, apologize, and patch the prompt. A bank cannot. The cost of a wrong answer is not a refund. It is a Consumer Financial Protection Act violation, a UDAAP claim, an OCC matter requiring attention, or a class action.

Three things make banking different:

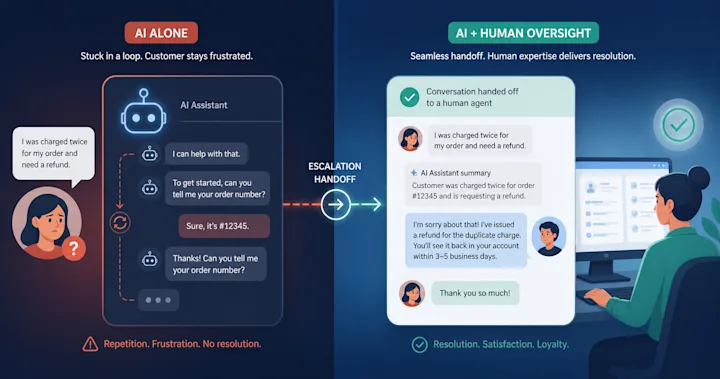

The customer is a consumer, not a buyer. CFPB rules apply the moment the AI touches a consumer financial product. The 2023 CFPB Issue Spotlight on chatbots in consumer finance was explicit: poorly deployed chatbots can trigger violations of federal consumer protection law, even if no human at the bank intended harm. The Moffatt v. Air Canada decision in 2024 made the legal exposure concrete in a different industry: the airline was held liable for a refund its chatbot invented. A bank chatbot that invents a fee waiver, a payment date, or an APR creates a comparable problem with worse downside.

The product is regulated, not just sold. A wealth management AI cannot tell a customer to “sell that fund” without becoming an investment adviser. A retail banking AI cannot tell a customer their loan was approved before underwriting signs off. A credit union AI cannot promise a refund that violates Regulation E or Regulation Z. The model has to know what it is allowed to say and confidently refuse the rest.

The audit trail is mandatory. Regulators expect institutions to explain how an automated decision was made, what data went into it, and whether the customer received accurate information. That is not a feature request. That is FFIEC and OCC table-stakes. AI that cannot produce a per-conversation audit log with sources, confidence, and decisions is not deployable in production banking.

This is why a generic AI chatbot ported into a bank rarely lasts a quarter. The same is true of “AI built for banking” tools that cannot ground every answer in the bank’s own approved sources. Grounded answers and audit logs are not nice-to-haves. They are the cost of entry.

The 2026 Regulatory Landscape, in One Page

You do not need to memorize the rules. You need to know which agency owns what so the right people sign off on the rollout.

Regulator or rule | What it cares about | What that means for your AI |

CFPB | Consumer protection, UDAAP, fair lending, dark patterns in chatbots | Bot must be accurate, transparent, and route to a human on request |

OCC | Safety, soundness, model risk, third-party risk | Vendor must support model risk management (MRM) and third-party reviews |

FFIEC | IT examination, information security, AI/ML supervision | Audit trail, change control, access management, vendor due diligence |

FINRA / SEC (broker-dealers, advisers) | Suitability, recordkeeping, communications with the public | All AI-customer interactions retained and reviewable; no unauthorized advice |

Regulation E | Electronic funds transfers and disputes | AI must respect dispute rights and timing rules |

Regulation Z | Truth in Lending | AI must not misstate APR, terms, or fees |

GLBA / state privacy laws | Customer data protection | Data minimization, encryption, consent, no training on customer data |

EU AI Act (where applicable) | High-risk AI in financial services | Risk management, transparency, human oversight |

Two patterns repeat across every one of these. The AI must be accurate against an approved source. The institution must be able to prove that after the fact. Get those two right and the rest is process.

7 Use Cases for AI Customer Service in Banking and Financial Services

These are the deployments that work in production today. They are ranked roughly by speed-to-value for a typical retail or commercial bank.

1. Self-service for account, fee, and product questions

The highest-volume queue in any retail bank is “where is X”: the routing number, the wire cutoff, the overdraft fee, the international transaction charge, the way to order new checks. A grounded AI chatbot trained against the bank’s actual policy library and knowledge base can resolve these questions in seconds, with a citation to the source page. This is the easiest 30-50% deflection most banks will ever get, and it does not require any change to underwriting, fraud, or core systems.

2. Authentication and intent capture in voice

A 2026 bank voice agent does two things well: it verifies identity using a defined set of factors, and it captures the customer’s intent in their own words before routing. That is enough to remove 60-90 seconds of friction from every call. It does not need to resolve complex requests on its own: it needs to hand off to a human or a downstream automation with the customer authenticated and the intent classified.

3. Agent assist for live calls and chats

This is the use case that most contact center leaders underestimate. AI sitting next to the agent (drafting responses, surfacing relevant policy, pulling the right disclosure language, summarizing the call when it ends) moves average handle time and first call resolution faster than any customer-facing bot. It also keeps the human accountable, which is exactly what compliance prefers. (See agent assist for the architecture pattern.)

4. Card disputes and Regulation E intake

Disputes are a legally structured workflow. The AI can collect the right information, classify the dispute type, run the initial fraud checks, and produce a complete case file for a human dispute analyst. It does not adjudicate. It does the front-end work, applies the correct timing rules, and escalates with everything the analyst needs in one place.

5. Loan and account application status

“What is happening with my loan?” is one of the highest-emotion tickets in retail and small business banking. An AI grounded in the loan origination system can give an accurate, current status and clear next steps without putting the customer on hold. It does not approve or deny. It tells the truth about where the application is in the pipeline.

6. Wealth management client servicing

For RIAs and wealth platforms, AI handles client servicing tasks that do not require advice: statements, performance reports, beneficiary updates, address changes, contribution windows, RMD reminders, tax document availability. The line is bright. The AI does not interpret performance, recommend allocation, or comment on suitability. It services the account and routes anything that smells like advice to a licensed adviser.

7. Fraud, identity, and account takeover triage

Fraud queues are time-sensitive and high-stakes. AI can triage fraud reports against patterns, place protective holds where policy permits, capture forensic detail from the customer in their own words, and escalate with a complete narrative to the fraud team. The human still owns the decision. The AI shaves minutes off every case at the front of the funnel.

A useful framing: in every one of these cases, AI handles the structured, high-volume, low-judgment work, and humans keep the judgment. That is the deployment pattern that survives a regulatory exam.

What To Look For in a Banking AI Customer Service Platform

The vendor landscape is loud. Glia announced CoPilot for Banking on March 30, 2026, joining a category that already includes Kasisto, Interactions, Posh, Eltropy on the credit union side, and the major contact center platforms (NICE, Genesys, Salesforce) shipping their own agentic features. On top of that, every horizontal AI support vendor (Ada, Forethought, Decagon, Sierra) has a banking case study somewhere on the website.

Cut through the noise with these requirements. If a vendor cannot demonstrate all of them in a 30-minute working session, they are not ready for a regulated environment.

Grounded answers, not generated answers. Every response has to be traceable to a specific approved source: a policy page, a knowledge base article, a backend record. Models that “synthesize” answers from training data have no place in banking customer service. Validated accuracy above 95% is the bar, not 80%. (IrisAgent’s Hallucination Removal Engine was built for exactly this constraint.)

Per-conversation audit trail. Every customer interaction needs to log the question, the retrieval results, the cited source, the confidence score, the model version, the response shown, and the human override (if any). When an examiner asks “how did the AI decide that?”, the answer is in the log.

Clear refusal behavior. The system has to know what it is not allowed to answer and respond cleanly: “I can’t give investment advice, but I can connect you with a licensed adviser.” Not “Here is what I think you should do.” Refusal is a feature.

Native integration with your stack. Most banks run on a combination of Salesforce Financial Services Cloud, Zendesk, Intercom, Freshdesk, or a homegrown contact center on top of a core (Fiserv, FIS, Jack Henry). The AI must install inside that workflow, not require a re-platform. The right answer is one click and a configuration screen, not a 6-month integration project.

Action, not just answers. Resolution means the ticket closes. A banking AI that can read account state, place a hold, schedule a payment, send a duplicate statement, or open a dispute case is doing the job. A bot that only links to a help article is a deflection tool, and deflection tools do not move CSAT or cost per ticket the way leadership wants.

SOC 2 Type II, no training on customer data, configurable data residency. These are baseline. If the vendor cannot show the report, document the data flow, and let your security team configure where data lives, walk away.

Per-agent or per-volume pricing you can model. Per-resolution pricing (Ada at roughly $3.50 per resolution, Intercom Fin at $0.99 per resolution) is hard to forecast and hard to explain to a CFO. Per-agent pricing scales with the team you already budget for. (See the pricing teardown for how to compare.)

Days, not quarters, to deploy. Decagon’s published deployment cycle is 6 weeks. Sierra’s enterprise floor is in the $150K-plus range. Forethought’s data minimum is 20,000 tickets. None of those should be acceptable in a category where the regulators are moving faster than vendors. IrisAgent deploys against an existing help desk in 24 hours and closes the first ticket the same day.

What Happens When Banks Get This Wrong

The cautionary tales are public, and they get expensive fast. Air Canada was held liable in 2024 for a chatbot that invented a bereavement refund policy. The case became the de facto reference point for “the company owns whatever its bot says.” The CFPB’s 2023 Issue Spotlight collected real consumer complaints about chatbots in finance trapping customers in loops, refusing to escalate to a human, and giving inaccurate answers about fees and disputes.

In a banking context, the same failure modes look like:

A chatbot promises a fee waiver. The system does not honor it. The customer sues, complains to the CFPB, or both.

A wealth chatbot answers a suitability question. The conversation gets surfaced in a FINRA exam.

A loan status bot tells a small business owner their application was approved before it was. They make a hiring decision against a loan that gets declined.

A dispute bot loses Regulation E timing because it never escalated to a human in the legally required window.

A voice agent records a customer without proper consent under a state two-party consent law.

None of these are AI mistakes. They are deployment mistakes. The right architecture, the right escalation rules, and the right audit trail prevent every one of them.

How To Deploy AI Banking Customer Service Safely

This is the playbook that survives a model risk review and a compliance audit. It is also the deployment that hits production faster, because the gates exist for a reason.

1. Start with intents that have one right answer

Routing numbers, branch hours, fee schedules, statement availability, card activation. These intents have an authoritative source and no judgment required. Get the AI accurate against your own approved content first. Resolve those intents before touching anything that involves account state.

2. Ground every answer in approved sources

The AI’s only allowed inputs for customer-facing answers are the bank’s policy library, knowledge base, product pages, and backend systems. Training data is not a source. If the model cannot cite where the answer came from, it does not send the answer. (See grounded AI for customer support for the retrieval pattern.)

3. Define the refusal list, not just the answer list

Document, in writing, the categories the AI is not allowed to answer: investment advice, tax advice, legal advice, anything that requires a licensed person, anything that touches an active fraud investigation. Build the refusal list before the answer list. It is shorter and it is more important.

4. Set confidence thresholds and escalation rules

Below a defined confidence score, the AI hands off to a human. Above it, the AI answers and logs. The thresholds are not magic: they come from a small validation set you build with your contact center and compliance team. (Most banks land between 0.70 and 0.85 after the first round of tuning.)

5. Make human handoff fast and stateful

Customers should never have to repeat themselves on handoff. The agent receives the conversation, the authenticated identity, the intent classification, and the AI’s draft response, with the source it cited. This is the single biggest predictor of CSAT in AI banking deployments.

6. Build the audit trail before launch, not after

Decide what gets logged, where it lives, how long it is retained, and who can query it. Run a tabletop exercise where compliance asks “show me every conversation where the AI mentioned a fee” and verify you can answer in minutes, not weeks. This is the conversation that examiners are going to have with you in 2027 and 2028.

7. Measure both AI and customer outcomes

Internal metrics that matter: containment rate (resolved without escalation), accuracy on the validation set, refusal precision, escalation handoff time. Customer metrics that matter: CSAT, NPS, complaint rate, regulator complaint rate, time to resolution. Track them all. (See the customer support metrics reference for definitions.)

8. Roll out by intent, not by team

Launch the routing-number flow before the fee-dispute flow. Launch fee-dispute before account-takeover triage. Each new intent is a small, contained release with its own success criteria. Banks that try to launch “the AI” across every queue at once are the same banks that rip it out a quarter later.

How IrisAgent Approaches Banking and Financial Services Support

IrisAgent is the AI support resolution platform that resolves more than 50% of tickets with grounded answers, no hallucinations, and a 24-hour deployment. For banks, credit unions, and wealth platforms, three architectural choices make it deployable in regulated environments.

The Hallucination Removal Engine validates every answer against the cited source before it sends. Validated accuracy stays above 95% across enterprise deployments, including Dropbox, Zuora, and Teachmint. In a regulated context, that means refusal is the default for anything outside the approved source set.

Native install on Zendesk, Salesforce (including Financial Services Cloud), Intercom, Freshdesk, Jira Service Management, and Zoho means the integration is a configuration step, not a project. Banks running on those platforms can be in production inside a single week.

Per-conversation audit trail with source citation, confidence score, model version, and human-override capture is built in, not bolted on. Compliance and model risk teams can pull the data they need without engineering tickets.

Pricing is per-agent, not per-resolution. That makes the budget conversation a simple model against current headcount, not a forecast against unknown ticket volume. (See the demo for a working walk-through against your own scenarios.)

What IrisAgent will not do, by design: give investment advice, give tax advice, answer regulated questions outside its allowed source set, send a response it cannot cite, or close a conversation a customer wanted escalated. Those are not limitations. Those are the controls that make AI deployable in financial services.

Final Takeaway

AI customer service in banking and financial services is no longer a question of whether. It is a question of how, and how fast. The institutions that get it right in 2026 will share three traits. They start with intents that have one right answer. They demand grounded responses, refusal behavior, and audit trails before they sign a contract. And they roll out by use case, not by team.

Your action list for the next 30 days:

Pick three intents with an authoritative source and no judgment required. Get them production-ready first.

Document the refusal list (the categories your AI is not allowed to answer) before you build the answer flows.

Require any vendor to demonstrate grounded retrieval, per-conversation audit trail, and 24-hour native install in a working session, on your data, before procurement opens.

Define your validation set with the contact center and compliance team. Decide what “good” looks like in numbers, then measure against it weekly.

The cost of doing this well is a quarter of focused work. The cost of doing it badly is a CFPB consent order or a viral failure. The right vendor makes the first path obvious.

See how IrisAgent deploys grounded AI customer service in regulated environments: 20 minutes, working demo against your stack.

Sources

Consumer Financial Protection Bureau, “Issue Spotlight: Chatbots in Consumer Finance” (June 2023)

Office of the Comptroller of the Currency, Bulletin on third-party model risk and AI/ML supervision

FFIEC IT Examination Handbook, sections on information security and outsourcing

Civil Resolution Tribunal,

Moffatt v. Air Canada

(2024): chatbot liability precedent

Glia, “CoPilot for Banking” launch announcement (March 30, 2026)

Allied Market Research, AI in Financial Services Market Forecast (AI agents in financial services projected to ~$6.54B by 2035)

IrisAgent customer deployments: Dropbox, Zuora, Teachmint

Frequently Asked Questions

Is AI customer service safe for banks and credit unions?

AI customer service is safe for banks and credit unions when every answer is grounded in approved sources, the system refuses regulated topics it is not qualified to answer, and every conversation produces an audit trail. Generic AI chatbots without those controls are not safe in a regulated environment, regardless of model quality.

What banking tasks should AI not handle in 2026?

AI should not handle investment advice, tax advice, legal advice, suitability decisions, underwriting decisions, fraud adjudication, or any decision that requires a licensed person. AI can prepare, triage, and capture information for those workflows, but a human or system of record makes the decision.

How does a banking AI chatbot stay compliant with the CFPB?

A compliant banking AI chatbot answers accurately from approved bank sources, never invents policy or fees, escalates to a human on customer request, never traps the customer in loops, and produces a per-conversation audit log. The CFPB's 2023 Issue Spotlight on chatbots in consumer finance lays out the specific failure modes to avoid.

What is the difference between AI for banking and generic AI customer service?

Banking AI customer service has to meet additional requirements: regulated refusal behavior, per-conversation audit trails, model risk management documentation, integration with regulated systems of record, and explicit boundaries around advice. Generic AI customer service can be brand-safe and accurate without meeting those gates. The architecture is similar; the controls are stricter.

How long does it take to deploy AI customer service in a bank?

Deployment timelines range from one week (native install into an existing Salesforce, Zendesk, or Intercom environment with grounded answers on a small intent set) to several months (custom integrations into a core banking system or contact center platform). Most retail and credit union deployments can resolve their first real ticket within 7-14 days when the vendor supports native install and grounded retrieval.

Should credit unions and small banks use the same AI vendor as megabanks?

No. Megabanks have model risk management teams, dedicated AI governance functions, and procurement cycles that fit 6-month vendor projects. Credit unions and community banks need vendors that deploy in days, price predictably, and ship the audit trail and refusal behavior in the box. The compliance bar is the same. The implementation surface is much smaller.