AI for Failed Payments and Transaction Disputes in Fintech

AI for failed payments and transaction disputes is an AI agent that resolves the tickets generated when money does not move as expected: a declined card, a failed transfer, a payment stuck in processing, or a charge the customer wants to dispute. It authenticates the customer, reads the actual transaction record and the decline or return reason, explains in plain language what happened, and either guides the fix or opens a properly documented dispute, while routing genuine fraud to a human. For fintechs this matters because payment-failure and dispute tickets are high-anxiety, high-volume, and directly tied to trust: a customer whose transfer failed and who cannot get a straight answer is a customer questioning whether their money is safe. IrisAgent resolves the routine cases end to end and escalates the regulated ones cleanly, so customers get answers in seconds without weakening your controls.

That is the headline. The rest of this guide is the operator's version: why payment-failure tickets are uniquely urgent, which ones to automate, the firm line around fraud and disputes, and what to measure.

Key takeaways - Payment-failure tickets are urgent in a way ordinary support is not, because the customer believes their money is stuck. Speed and a clear explanation are the whole job. - The four workflows worth automating first: declined-card explanations, failed-transfer recovery, payment-status checks, and structured dispute intake. - The AI explains and recovers routine failures and opens well-documented disputes. It does not adjudicate fraud or decide a chargeback outcome. Those stay with your risk and compliance teams. - Grounding is non-negotiable: the AI must read the real transaction record and the actual decline or return code, not guess from a generic FAQ. - Track three numbers: payment-failure resolution rate, dispute intake completeness, and repeat-contact rate on failed payments.

Why failed-payment tickets are the most urgent queue in fintech

When a SaaS user cannot find a setting, they are annoyed. When a fintech customer's transfer fails or a card is declined at the checkout, they are scared. They think their money is gone, their rent payment bounced, or their account is frozen. That fear drives an immediate, often repeated contact, and it drives churn faster than almost anything else in financial services.

The cruel part is that most of these failures are mundane and explainable. A card declines because of an issuer rule, an insufficient balance, or an expired card. A transfer fails because of an ACH return code, a daily limit, or a mismatched account detail. A payment sits in processing because of a normal settlement window. Each of these has a clear, factual answer sitting in the transaction record. The customer just cannot see it, and a slow support queue means they stew in uncertainty.

This is a support problem with a trust multiplier. The verification engine, the card network, and the ledger are all doing their jobs. What is missing is the layer that reads the failure and explains it to the customer instantly, in plain language, before fear turns into a closed account.

The cost-of-doing-nothing math

Failed-payment tickets are expensive twice. First in support load, because the anxiety drives repeat contacts: the same customer messages three times in an hour. Second in churn, because a customer who cannot trust that their money moves reliably leaves. For a fintech acquiring customers at real cost, losing them to an unexplained decline is a double loss, the acquisition spend and the lifetime value, over a problem that was usually a one-line explanation.

A human team cannot answer fast enough at the moment of panic. AI can, responding in seconds with the actual reason and the specific next step, which is what defuses the fear before it becomes an exit.

The four payment-failure workflows worth automating first

Start with the high-volume, explainable failures that do not require a fraud analyst.

1. Declined-card explanations

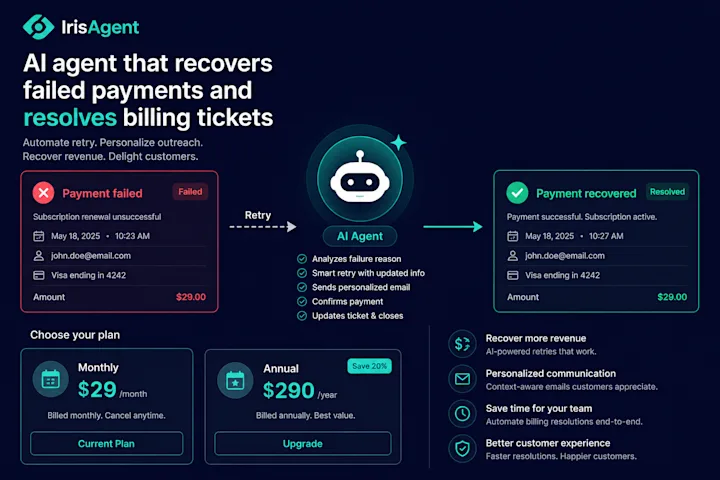

"Why was my card declined?" is one of the highest-volume fintech tickets. The AI reads the decline reason from the transaction record and explains it precisely: insufficient funds, an issuer block, an expired card, a velocity limit, and gives the exact fix. Most resolve with a clear explanation, no human needed. This connects to the card activation use case for the setup-stage version of the same problem.

2. Failed-transfer recovery

A failed transfer is high-anxiety because the customer cannot see where their money went. The AI reads the return code, explains whether the funds bounced back or never left, and walks the customer through the correct fix: updating account details, retrying within limits, or waiting out a settlement window. This is the core of the automate failed transfers use case.

3. Payment-status checks

"Where is my payment?" generates a steady stream of repeat contacts during normal settlement windows. The AI checks live status against the ledger and gives a straight answer: settled, processing, returned, or pending, removing the uncertainty that drives the customer to message again and again.

4. Structured dispute intake

When a customer wants to dispute a charge, the quality of the intake determines the outcome. The AI runs a structured, complete intake: it identifies the transaction, captures the dispute reason against the right framework, gathers the required evidence, and opens a properly documented case, so the dispute is ready for review instead of a half-filled form. This is the support-side work in the transaction disputes use case. For the refund-processing mechanics that often follow, see the guide on AI refund automation for returns and billing disputes.

The firm line: support versus the fraud and dispute decision

This is the part that separates a safe deployment from a dangerous one.

The AI explains failures and opens disputes. It does not decide them. It does not adjudicate whether a transaction was fraudulent, it does not approve or deny a chargeback, and it does not override your risk controls. Those are regulated risk and compliance functions, governed by card-network rules, ACH frameworks, and consumer-protection expectations like the CFPB's 2023 guidance on chatbots in consumer finance. The same boundary discipline applies here as in KYC and identity verification support: the AI does the legwork, the human owns the regulated judgment.

What the AI does is make the human's job faster and the customer's experience better: it resolves the routine failures that never needed a human, and for the cases that do, it hands a fraud or dispute analyst a complete, structured case instead of a vague ticket. When a transaction looks like genuine fraud, the AI does not improvise or reassure. It escalates immediately to a specialist with the full record, the same way agent assist is designed to work.

Get this line right and AI cuts your payment-failure queue while strengthening your dispute and fraud process. Get it wrong and you have automated a liability. The architecture has to enforce the boundary, not a prompt.

What "AI resolves a payment failure" looks like end to end

Here is the workflow for a customer whose transfer just failed.

Trigger. The transfer returns a failure, or the customer messages "my transfer didn't go through."

Authentication. The AI matches the customer to their account and pulls the specific transaction record.

Failure decoding. The AI reads the return or decline code and the transaction metadata, then explains in plain language what happened and where the money is.

Guided recovery. The AI gives the exact fix for that failure type and confirms when a retry succeeds.

Escalation if needed. If the case looks like fraud or a genuine dispute, the AI opens a structured, fully documented case and routes it to a specialist. It never adjudicates itself.

The customer goes from panic to a clear answer in seconds, at any hour, on the routine cases that make up most of the queue. This is the same agentic capability the AI customer support for financial services and fintech page describes, applied to the moment customers trust you least.

What to measure

Three numbers tell you whether payment-failure automation is working.

Payment-failure resolution rate: the share of declined-card, failed-transfer, and status tickets the AI closes without a human. Watch this climb as the AI learns your decline and return codes.

Dispute intake completeness: the share of disputes that reach review with all required evidence and the correct reason code on the first pass. Better intake means faster, more winnable disputes.

Repeat-contact rate on failed payments: how often the same customer contacts again about the same failure. Falling repeat contacts is the clearest sign the explanation actually landed and the fear was defused.

Model the impact of a faster, more trusted payment-failure queue with the ROI calculator.

How payment-failure AI fits the rest of your fintech support stack

Failed payments and disputes are one slice of fintech support. The same AI agent that explains a declined card also recovers a stuck onboarding at KYC, activates a new card, and answers account questions, all from the same knowledge and integrations and all behind the same compliance boundary. The strategic picture of where AI fits across the regulated fintech support journey lives on the fintech support AI hub, and the broader product capability is covered on the AI for customer support page.

Get the payment-failure queue right and you protect the thing fintech runs on, which is trust that money moves reliably and questions get answered fast.

Frequently Asked Questions

What payment-failure tickets can AI resolve automatically?

Declined-card explanations, failed-transfer recovery, and payment-status checks are the highest-volume categories, and AI resolves them end to end when it reads the actual transaction record and decline or return code. For disputes, the AI runs a structured intake and opens a documented case, while the decision stays with your risk team.

Does AI decide chargebacks or fraud cases?

No. The AI explains failures and opens well-documented disputes, but it does not adjudicate fraud or decide a chargeback outcome. Those are regulated risk and compliance functions that stay with your specialists, governed by card-network rules and consumer-protection guidance. Genuine fraud is escalated immediately with the full record.

How does AI reduce churn from failed payments?

It responds at the moment of panic. When a transfer fails or a card is declined, the AI immediately explains what happened and where the money is, in plain language, instead of leaving the customer to fear the worst while a slow queue catches up. That instant, factual answer is what keeps a scared customer from closing the account.

What systems does this work with?

The approach integrates with your ledger, card processor, and transfer rails through their APIs to read transaction status, decline reasons, and return codes, then layers the explanation, recovery guidance, and structured dispute intake on top.